When Shares Determine Control: A Founder Lesson in Startup Governance

In startups, it is often assumed that decisions are made by the people around the table. Founders, managers, and partners discuss, align, and move forward together. At least, that is the intention. In practice, something else determines who is really in charge: the ownership structure. This is my founder story about how control can shift — not through conflict or disagreement, but through shares, clauses, and conditions that seemed reasonable at the time. It illustrates how equity does not just define who benefits from success, but who ultimately decides what happens along the way. In this context, it helps to distinguish between shares and equity. Shares are the individual units of ownership in a company. Equity is the percentage of the company those shares represent — in other words, how much of the company you effectively own. And how, once that structure is in place, even well-founded arguments and technical expertise may no longer be enough to influence the outcome.

The Initial Setup: Shared Intentions, Unequal Structures

At the outset, nothing suggested that control would ever become an issue. We were a small group of people who believed in the same idea and, at least in our own minds, were working towards the same goal. The conversations we had were open, constructive, and focused on how to move the technology forward and turn it into something that could work in practice. Decisions were discussed, arguments were weighed, and there was a general sense that we would figure things out together.

In that phase, we thought in terms of collaboration, not control. The implicit assumption was that decision-making would follow from involvement: those who contributed would naturally have a say. That felt logical and fair, and it matched how we had worked in academic and technical environments before, where content and expertise tend to carry weight.

At the same time, a formal structure was being put in place. Shares were allocated, roles were defined, and agreements were drafted to support the formation of the company. The collaborating university, which provided the patented technology, received a small percentage of the shares in exchange for granting a license to use it, as I described in another page about our first time founder adventure. Yes, we were involved in those discussions, but our focus was not on the precise implications of each clause or percentage. The structure was something that needed to be arranged, but it did not feel like the core of what we were building. The technology and its application were.

Looking back, that was where the imbalance started to take shape. While we were primarily thinking about the content — the idea, the technology, and how to make it work — the structure of ownership was being defined in parallel. And that structure does not describe how people intend to work together; it defines what happens when intentions are no longer aligned.

At the time, however, there was no visible tension between those two layers. Our intentions were aligned and shared, the atmosphere was positive, and the formal distribution of shares did not seem to contradict that. It simply existed alongside it. Only later did it become clear to me that this structure had followed a logic of its own, in which earlier contributions — such as technology and intellectual property — were already being translated into ownership. How that process works, and why it has such a lasting impact, is explained in more detail in this page on how intellectual property becomes shares.

Only later I began to understand that these were not two separate things. The ownership structure was not just a background detail. It was the mechanism that would ultimately determine how decisions were made — especially in situations where agreement was no longer automatically attained. This founder lesson illustrates one of the most important principles discussed in our guide to Co-founder Dynamics: decisions about ownership and control made at the beginning of a startup can have consequences for many years and even the ultimate faith of the company.

Bringing in Experience: A Logical Step Forward

As the idea started to take shape beyond the purely technical domain, we became increasingly aware that building a company would require a different kind of experience. We understood the technology and its potential, but turning that into a functioning business was something we had not done before. It felt entirely reasonable — almost necessary — to bring in someone who had.

I took the initiative to find that experience. Through my network, I identified a manager with a strong track record and approached him directly. He was capable, convincing, and seemed to understand both the ambition and the complexity of what we were trying to build. At that stage, I still saw a clear role for myself in the future company — possibly in a CEO-like position, or at least in close collaboration with him. The idea was to complement each other, not to replace one another.

Around the same time, there was another experienced entrepreneur in our local network — someone I had known for much longer. I introduced the two of them for a very practical reason: the manager I had brought in was not familiar with our regional ecosystem, and I thought it would be useful for him to get to know people locally. That was the extent of it. It was not intended as a step towards forming a joint management structure.

In my mind, the situation was still straightforward. We were bringing in experience to strengthen what we were building, not to redefine who would be building it. The expectation remained that we would develop the company together, combining our technical expertise with the entrepreneurial experience we were adding.

Then, for a few weeks, things went quiet.

When we heard back, the situation had shifted. The two of them had been in contact, talked a lot, and had come to the conclusion that they would take on the management of the company together. They presented this as a logical step forward: a strong, experienced team that could take responsibility for building and scaling the business.

From their perspective, this made sense. From ours, it was less straightforward. The idea that we would “do this together” was still there, but its meaning had subtly changed. What we had initially seen as adding experience to the team was now becoming a situation where that experience started to define the structure of the team.

And at that moment, I realized that my own role was no longer as clearly defined as I had assumed. The expectation of a shared leadership structure — or even a joint CEO role — was no longer implicit. It had been replaced by something more structured, and, although not yet fully explicit at that moment, more hierarchical. My two fellow founders did not seem overly concerned about the shift. They laughed it off and made a passing remark that having a strong management team was probably a good thing. I saw it somewhat differently. What appeared to be a practical step forward also implied a change in roles — one in which my own position was becoming less clearly defined. At that stage, this shift was not yet formalized. It was more a change in direction than in structure. But it set the stage for what followed, where these evolving roles would be translated into concrete agreements — and, ultimately, into a different distribution of shares.

We (and I) accepted this development, partly because the reasoning sounded plausible, and partly because we were still focused on moving forward. But in hindsight, this was an early indication that bringing in the experience of a seazoned does not only add capability — it can also reshape expectations about control and decision-making, often faster than you realize.

The Clause That Changed Everything

As the plans for the company became more concrete, the discussions gradually shifted from ideas and roles to formal agreements. Shares were allocated, responsibilities were outlined, and the structure of the company was put on paper. This was all part of the natural progression from concept to organization. We were involved in these discussions, but, as before, our primary focus remained on the content — the technology and its application.

Somewhere in that process, a clause was introduced that, at the time, did not stand out as particularly significant. It stated that if the management team succeeded in bringing in a substantial assignment or investment, they would be entitled to additional shares. The underlying logic seemed reasonable: if they were able to accelerate the company by securing external funding or commercial traction, it would justify a larger stake.

We did not spend much time analyzing the exact implications of that clause. It felt conditional, almost hypothetical — something that might or might not happen in the future. And even if it did, we assumed it would be part of a broader, shared success. The idea that such a condition could materially shift the balance of ownership did not fully register at that point.

What we also did not anticipate was how quickly the condition would be met.

Within a relatively short time, the management team secured funding through a government program. Formally, this was structured as an “assignment.” In practice, it functioned much like a subsidy. But from a contractual perspective, it satisfied the condition that had been defined in the agreement.

And with that, the clause was triggered.

Additional shares were allocated. The ownership structure changed. Not dramatically in appearance — the percentages shifted by what seemed like a limited margin — but fundamentally in terms of what it meant.

What had previously been a relatively balanced distribution of shares now moved towards a situation where the management team held a majority. At that moment, nothing else visibly changed. The same people were involved, the same conversations were taking place, and the same plans were being discussed.

But the underlying structure had shifted in a way that would later prove decisive.

When Majority Means Control

It was only after the clause had been triggered and the shares had been reallocated that the implications started to become clear. Not immediately, and not through a single moment, but gradually — through how decisions were made, or more precisely, how they were no longer made.

On paper, the situation was straightforward. The two members of the management team each held a significant percentage of the shares. Together, they now formed a majority. I held a smaller stake. The distribution itself did not look dramatic at first glance, but it crossed an important threshold: they could outvote us.

At the time, we did not think in those terms. We still approached discussions as if they were collective. We explained our reasoning, raised concerns, and expected that arguments would be evaluated on their merits. That had been the pattern until then, and there was no explicit moment where someone said: “from now on, we decide.”

But in practice, the dynamic had already changed.

Decisions increasingly reflected the perspective of the management team. Not because they were imposed abruptly, but because the structure allowed them to be. When there was alignment, nothing seemed different. But when there was disagreement, the outcome was no longer open-ended. The possibility of being overruled had become real — and, over time, it became the default.

We found ourselves in a position where we were still involved, still contributing, still part of the discussions — but no longer decisive. The shift was subtle in how it appeared, but absolute in what it meant. Ownership had crossed the point where influence turns into control.

In formal terms, the situation was clear: majority shareholders determine the outcome. But what is less obvious, especially in the early stages of a startup, is how quickly that principle starts to shape everyday decisions. It does not require conflict or confrontation. It simply follows from the structure that has been put in place.

Looking back, that was the moment where the company effectively changed hands — not through a transaction, but through a shift in percentages that we had not fully appreciated at the time.

Responsibility, Risk — and the Justification for Control

From the perspective of the management team, the situation was not only logical, but necessary. As they took on the roles of CEO and CFO, they positioned themselves as the ones responsible for the company's direction and performance. If things went wrong, they argued, they would be the ones held accountable — by partners, by funders, and ultimately by the outside world.

That sense of responsibility was directly linked, in their reasoning, to control. In their view, it was not acceptable to carry full responsibility without having the ability to make final decisions. And in a company structure, that ability is not defined by intention or discussion, but by ownership. Control, in practical terms, meant holding a majority of the shares.

Otherwise, as they explained, they would be in a position where they were accountable for outcomes they could not fully determine. That was a risk they were not willing to take. Framed in that way, the argument was difficult to dismiss. It aligned with how experienced operators tend to think about leadership: responsibility and authority need to be matched.

At the time, we accepted that logic. It sounded reasonable, and it fit with our broader goal of moving the company forward. We were still thinking in terms of collaboration, assuming that shared intentions would continue to guide decisions, even if the formal structure had shifted.

Looking back, the logic itself was not the issue. The connection between responsibility and control is real, and in many situations, justified. What we did not fully grasp was how that abstract reasoning translated into a concrete and irreversible distribution of power.

Once that link is formalized in shares and agreements, it no longer operates as a principle — it becomes a mechanism. And that mechanism determines who ultimately decides, regardless of how decisions were originally intended to be made.

The shift, in other words, was not presented as a transfer of control. It was presented as a requirement for responsible management. But in practice, the outcome was the same.

When Control Overrides Expertise

The consequences of that shift in control did not become visible all at once. In the beginning, the discussions continued much as before. Ideas were exchanged, technical options were explored, and there was still a sense of collaboration. But over time, a pattern started to emerge — not in how we talked, but in how decisions were ultimately made.

As the development progressed, the technical complexity increased. Choices had to be made about design, feasibility, and the sequence in which challenges would be addressed. From our perspective, some of these choices introduced unnecessary risk. We had concerns about combining too many uncertainties at the same time, especially in a system that was already difficult to make work under controlled conditions.

We raised those concerns repeatedly. The discussions were substantive and, at least on the surface, taken seriously. But the outcome of those discussions was no longer determined by the strength of the arguments alone. The underlying ownership structure had already defined who had the final say.

In practice, this meant that decisions increasingly reflected a single perspective — one that was more focused on speed and ambition than on technical robustness. Multiple risks were taken simultaneously in the development process. Each individual step might have been defensible, but in combination, they created a level of complexity that became difficult to manage.

In this case, those decisions led to increasing technical complexity. Multiple uncertainties were addressed at the same time, rather than being reduced step by step. This is often referred to as stacking technical risk, and it is rarely a good idea — for more than one reason.

This is also where the earlier shift in control started to have very concrete consequences. The choice to pursue a more ambitious, but riskier, technical path was not just a technical decision — it was enabled by a decision-making structure in which those concerns could ultimately be overruled.

From an external perspective, it makes a company much harder to evaluate. Investors, for example, tend to step back when too many unknowns are combined, as I describe in another founder case on stacking technical risk. But here we faced another, more immediate, practical problem:

When multiple risks are combined into a single system, failure becomes difficult to interpret. If the device does not work, it is no longer clear which part is responsible. Is it the sensing mechanism, the fluid handling, the electronics, or the interaction between them? Each component may be complex on its own, but in combination they create a system where cause and effect are no longer easy to trace.

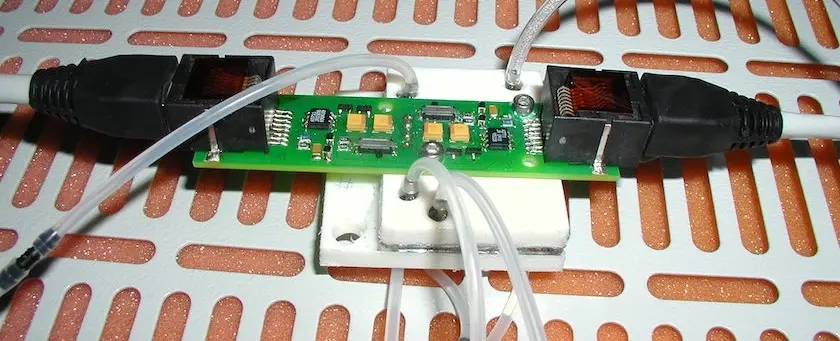

And that is exactly what happened in our case. At the core of the device (see the photo above) was a promising concept that, in isolation, could be understood and tested. But around it, a complex setup had developed — a network of tubing, fluid pumps, gas compartments and electronics that all had to function together. When the system failed to perform as expected, we could no longer isolate the problem. The complexity had become a barrier to progress.

At that point, improving the system was no longer a matter of solving a defined problem. It became an exercise in navigating uncertainty without clear feedback — a situation that is difficult to recover from, even with significant effort.

At a certain point, the dynamic became explicit. When we, the founding researchers, continued to question specific technical directions, the response was no longer primarily about the content of the argument. It was framed in terms of roles and authority: they were in charge, and therefore they would decide.

That moment made something clear that had been implicit for some time. Expertise still had a place in the discussion, but it no longer had the power to influence the outcome if it conflicted with the direction chosen by those in control.

In hindsight, the issue was not simply that different choices were made. The issue was that the structure no longer allowed for a meaningful correction. In a technically complex project, where uncertainty is inherent and feedback is essential, that absence of corrective capacity from the research side turned out to be critical.

The device never reached a working state.

What This Case Teaches Founders About Equity and Control

Looking back, nothing in this case was exceptional in a legal or procedural sense. The agreements were clear, the conditions were met, and the people involved acted in ways that, from their own perspective, were rational and defensible. And yet, the outcome was not what we had intended when we started.

The key lesson is that equity is not just about sharing future value and how many you can earn with the company is sold. It is about structuring control in the present. Here and now. Shares determine who benefits if things go well, but more importantly, they determine also who decides what happens along the way.

In early-stage startups, this distinction is easy to overlook. The focus is often on the idea, the technology, and the opportunity. Ownership structures are put in place alongside that process, but they tend to receive less attention — especially when intentions are aligned and trust is high. It feels natural to assume that collaboration will continue as it started.

What this case shows is that intention and structure operate on different levels. Intentions describe how people expect to work together. Structure defines what happens when those expectations are tested. And it is the structure that prevails.

A second lesson is that relatively small changes in shareholding can have disproportionate effects. Moving from a balanced distribution to a majority position does not simply increase influence — it fundamentally changes who has the final say. That shift may not be immediately visible in day-to-day interactions, but it becomes decisive the moment there is disagreement.

Finally, this case illustrates that control also affects the quality of decision-making. In complex, technology-driven projects, progress depends on the ability to challenge assumptions, adjust direction, and correct course when needed. When control is concentrated in a way that limits that feedback, the risk is not only financial — it becomes technical.

For founders, the practical implication is straightforward, but not always easy to act on: understand the ownership structure you are creating, not just in terms of percentages, but in terms of what it allows and what it prevents. Ask not only who owns what, but who decides when it matters.

Because in the end, it is the distribution of shares that determines who is in control. And while we often refer to this more broadly as equity, in practice it comes down to who holds how many shares — and what those shares allow them to decide. That structure does not just influence the outcome of a successful company. It determines the path the company takes — and whether it gets there at all.

A final lesson from this case relates to the composition of the startup team. In technology-driven ventures, it is often assumed that strong management should take the lead, while technical founders focus on the content. In practice, the distinction is not that simple.

Building a high-tech company does not only require managerial experience. It requires an understanding of what it means to develop new technology under uncertainty — and a willingness to engage with the people who work on that complexity every day. Decisions about direction, timing, and risk cannot be made effectively without that input.

This does not mean that the most technically focused founders should necessarily run the company. But it does mean that those in management positions need to be able to recognize when technical constraints matter, and to take them seriously in decision-making. Without that, there is a real risk that decisions are made that look reasonable on paper, but are not viable in practice.

In our case, that balance was lost. And once it was lost, the structure of control together with the personalities of the management team made it difficult to restore.

For a more detailed look at how to think about roles and balance within a founding team, see how to build an effective startup team.

This personal story is one of several real-world founder experiences featured on Technoventure. If you enjoy practical lessons from entrepreneurs, inventors and startup founders, explore our Founder Lessons collection.